Table of Contents

- Selecting the Right Merchant Services Provider for Your Small Business

- Understanding Merchant Services and Payment Processing

- Evaluating Costs, Cash Discount Programs, and Omnichannel Capabilities

- Steps to Select and Transition to a Merchant Services Provider

- Advanced Considerations: Compliance, Standards, and Optimization

- Frequently Asked Questions About Merchant Services

- Your Partner for Better Payment Processing

Selecting the Right Merchant Services Provider for Your Small Business

Choosing the right merchant services provider for small business is critical for controlling costs and delivering a smooth checkout experience. As you evaluate partners, focus on hardware flexibility, transparent pricing, and responsive support to keep your business running efficiently.

- Free or discounted Clover hardware: Look for a provider that offers free or discounted Clover hardware placement, subject to merchant qualification and approval, to minimize upfront costs.

- Integrated POS solutions: Ensure the provider supplies integrated POS platforms tailored to your business type—full-service restaurant, counter-service, retail, mobile, or e-commerce—to streamline operations.

- Competitive processing rates: Evaluate credit card processing for small business rates without hidden fees, monthly minimums, or long-term contracts, so you keep more of each sale.

- Cash discount program: Consider a cash discount program for small business that allows you to offset processing costs legally and transparently.

- Same-day setup and next-day funding: Prioritize providers that offer same-day setup and next-day deposits to maintain cash flow and avoid downtime.

- PCI compliance and security: Verify the provider adheres to strict payment industry standards and PCI DSS requirements to protect customer data.

- Dedicated support: Choose a partner with accessible, award-winning support rather than a generic call center.

- No cancellation penalties: Avoid agreements with cancellation fees or mandatory equipment leases; seek transparent terms.

For instance, POS Brokers offers no cancellation fees, free Clover placements for qualifying merchants, and a cash discount program.

Use this checklist to confidently select a merchant services provider for small business that matches your needs. For tailored hardware and rate recommendations, contact our payment specialists.

Understanding Merchant Services and Payment Processing

When evaluating payment solutions, it’s critical to understand the difference between a full-service merchant services provider for small business and a basic payment processor. A merchant services provider delivers end-to-end payment acceptance, including POS hardware like terminals, card readers, and accessories, merchant account setup and underwriting, ongoing support, and transparent pricing models. In contrast, a payment processor is a technical service that routes transaction data between a merchant’s terminal and the acquiring bank, with no provision of hardware or direct account management.

The following table outlines these distinctions.

| Aspect | Merchant Services Provider | Payment Processor |

|---|---|---|

| Scope of Services | End-to-end payment acceptance, POS hardware, software, merchant account, and support | Transaction routing and data transmission only |

| Hardware Provision | Supplies and supports POS terminals, card readers, and accessories | Often limited; may not include POS hardware or integration |

| Account Management | Maintains merchant accounts, underwriting, and compliance | Provides connectivity to acquiring banks; minimal account support |

| Pricing Model Transparency | Detailed interchange-plus, tiered, or cash discount options with disclosures | May obscure markup within the processing rate |

| Integration Support | Pre-built integrations with POS software and e-commerce platforms | API access only; merchant handles development and integration |

While a payment processor might offer a portal like Square Dashboard Login for basic transaction reporting, it lacks the integrated hardware, account management, and personalized support that a comprehensive merchant services provider supplies. At The POS Brokers, we cover every aspect: from your Clover POS system and merchant account to ongoing guidance. Our team supplies and supports Clover terminals, card readers, and accessories, including free placements for qualifying merchants (eligibility requirements apply). We handle the underwriting and compliance of your merchant account, ensuring a smooth setup and ongoing management that goes far beyond a processor’s minimal support.

Our credit card processing for small business solutions feature transparent interchange-plus and tiered plans with no hidden fees. We also offer a cash discount program for small business that helps you reduce processing costs legally—by offering a discount to customers who pay with cash or debit—while remaining fully compliant with card network rules. As our embedded payments guide explains, integrated payment solutions eliminate external gateways and reduce cart abandonment, benefits that are built into our full-service offering. Pre-built integrations with Clover POS software and e-commerce platforms save you from the complexity of handling API integrations yourself.

Understanding these differences helps you evaluate which partner can truly support your business’s growth. As you consider pricing models in the next section, remember that a full-service provider delivers not just transaction processing but a complete payment ecosystem—hardware, support, transparency, and the expertise to keep your operations running smoothly.

Evaluating Costs, Cash Discount Programs, and Omnichannel Capabilities

After negotiating your terms, the next step is to understand how your merchant services provider for small business structures pricing. The right model can protect your margins and support growth. We’ll break down traditional pricing, show how a cash discount program eliminates processing fees, and explain why unified omnichannel acceptance matters.

The following table contrasts a traditional pricing approach with a cash discount program to help you see the key differences.

| Aspect | Merchant Services Provider | Payment Processor |

|---|---|---|

| End-to-end payment acceptance, POS hardware, software, merchant account, and support | Transaction routing and data transmission only | |

| Supplies and supports POS terminals, card readers, and accessories | Often limited; may not include POS hardware or integration | |

| Maintains merchant accounts, underwriting, and compliance | Provides connectivity to acquiring banks; minimal account support | |

| Detailed interchange-plus, tiered, or cash discount options with disclosures | May obscure markup within the processing rate | |

| Pre-built integrations with POS software and e-commerce platforms | API access only; merchant handles development and integration |

A cash discount program shifts processing costs to card payers while keeping cash transactions fee-free, but it demands rigorous compliance. The POS Brokers helps you assess eligibility and supplies compliant solutions integrated with Clover, Lavu, and Revel—no third-party bolt-ons required.

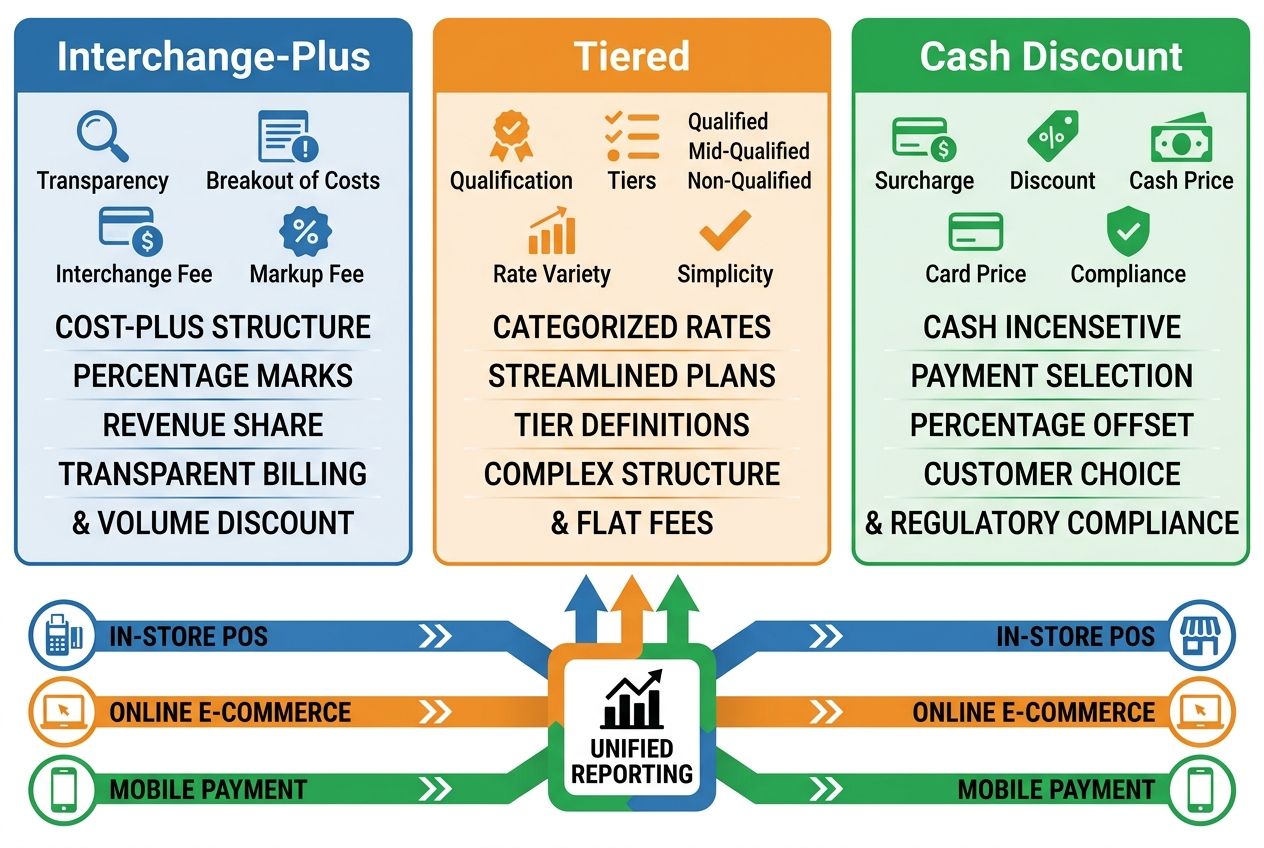

Comparison of payment processing pricing models and omnichannel acceptance visualization.

Comparing Pricing Models: Interchange-Plus, Tiered, and Cash Discount

When evaluating credit card processing for small business, interchange-plus is often the most transparent model. The business pays the interchange fee set by the card networks plus a small, fixed processor markup; total per-transaction costs typically land in the 2.5%–3.5% range. Tiered pricing, by contrast, groups transactions into qualified, mid-qualified, and non-qualified buckets, which can obscure exactly what you’re paying. For many small business owners, a cash discount program eliminates processing fees entirely. You display the cash price and apply a service fee to card payments—a model that differs from surcharging, where a fee is added on top of the listed price.

Implementing a Cash Discount Program for Your Small Business

A cash discount program for small business starts with a few practical steps. First, you post dual pricing signage at the entrance and the point of sale, so customers see both the cash price and the card-plus-service-fee equivalent. Your POS system must be configured to apply the fee automatically; solutions like Clover, Lavu, and Revel support this natively. To stay compliant, your checklist should include:

- Confirm state eligibility (not all states permit the program; our team verifies this for you).

- Post clear dual pricing notices at every checkout.

- Update your POS software with cash discount settings and test the fee calculation.

- Educate your staff on how to explain the program to customers.

- Print both prices on receipts for full transparency.

Cash discount programs can coexist with loyalty offers when your POS integrates both features. We provide compliant, turnkey solutions that work with your existing hardware, removing the need for bolt-on applications.

Enabling Omnichannel Payment Acceptance

Once your pricing is optimized, unifying all sales channels is the logical next step. An omnichannel approach syncs in-store POS, online payment gateways, and mobile payments into one merchant ecosystem. Integrated POS systems—Clover, Lavu, Revel—give you native omnichannel capabilities like real-time inventory sync and unified customer profiles, so you avoid fragmented reporting. Unified reporting dashboards similar to what you’d see with a Square Dashboard Login are essential for tracking sales across all channels. We help you connect every touchpoint so you can manage your business from a single platform.

When you’re ready to evaluate your options, we help small businesses compare pricing models and implement compliant cash discount programs that fit their operations. Reach out to see how our fully integrated merchant services can support your growth.

Steps to Select and Transition to a Merchant Services Provider

Selecting a merchant services provider for small business involves more than just comparing rates. A thoughtful evaluation and a smooth transition can save you from costly downtime and hidden fees. At The POS Brokers, we simplify that process with transparent pricing, free hardware placements, and dedicated support.

Evaluating Merchant Services Providers Against Your Business Needs

When evaluating a merchant services provider for small business, start with a checklist that covers these essential areas:

- Transparent pricing: Look for providers that offer wholesale rates with no hidden monthly markups and No Cancellation Fee. Affordable credit card processing for small business means you keep more of every sale.

- Hardware options: Determine whether the provider offers free or discounted terminals, such as our Free Clover Placements for qualifying merchants.

- Support quality: Verify availability of 24/7 support so you can get help whenever you need it.

- Cash discount program: Choosing a provider that supports a cash discount program for small business can offset processing costs by passing card fees to customers who choose to pay by card.

- System integrations: Ensure the provider can integrate with your existing accounting, inventory, and e-commerce platforms. Compatibility avoids manual data entry and errors.

At The POS Brokers, we help you check every one of these boxes — from no-cancellation-fee contracts to seamless integration support.

The following table outlines the POS platforms we supply, helping you match the right system to your business type and growth plans.

| Feature | Traditional Pricing | Cash Discount Program |

|---|---|---|

| Processing Fees | Business pays interchange plus processor markup, typically 2.5% – 3.5% per transaction | Fees are shifted to the customer who chooses to pay by card; cash customers pay the listed price |

| Surcharge | Additional surcharge rules vary by state; surcharges add a fee on top of the price | No surcharge model – price displayed is the cash price; a service fee is applied to card payments |

| Customer Cost | All customers pay the card price regardless of payment method | Card-paying customers see a small fee; cash customers pay the advertised price |

| Compliance Requirements | Standard card brand rules for surcharging, require signage and registration | Must follow cash discount rules: post dual pricing clearly, ensure POS software supports the program |

This variety ensures that whether you run a boutique or a multi-store chain, you’ll find a solution that fits.

Once you’ve identified the right provider, follow these steps to transition smoothly.

Seamlessly Switching Merchant Services Providers

Transitioning to a new processor doesn’t have to disrupt your business. We handle the heavy lifting so you can focus on running your business. Follow this migration checklist to avoid downtime:

- Sign your new merchant agreement with us — we configure your account and assign a dedicated support contact.

- Request porting of compatible terminals: If you’re using Clover devices that are eligible, we can reprogram them so you avoid purchasing new hardware.

- Schedule the cutover for a low‑volume day or after hours. We help you time the switch to minimize transaction disruption.

- Test everything: Run test transactions and verify that all integrations — accounting, inventory, e‑commerce — are functioning before you go live.

- Cancel the previous merchant service only after the new system successfully processes a live transaction. This ensures you never experience downtime.

Our support team is available 24/7 to guide you through the entire migration. And because we never charge a cancellation fee, you’re free to switch whenever you’re ready.

Pro tip: keep your old system running until you confirm the new setup works flawlessly. If you’re moving from Square, use our guide on the square dashboard login to export your transaction history and customer records. Our team can assist with data migrations from platforms like Square, using the steps we’ve documented in our internal FAQ. The entire migration process typically takes just a few days, and we provide step‑by‑step guidance every step of the way.

Securing Free POS Hardware and Accelerated Funding

Qualifying merchants can take advantage of free Clover hardware and accelerated funding programs. According to our internal support documentation, eligibility is based on your processing volume and credit history, and we assess this during your application. For approved accounts, we offer same‑day setup: if your application is submitted and approved before our shipping cutoff, we can configure your account and ship the hardware the same day (subject to carrier availability). Next‑day funding ensures that settled funds reach your bank account the business day after batch settlement, improving your cash flow. Free hardware placements are exclusive to Clover systems; for other POS platforms, we provide discounted options. As your partner for better payment processing, The POS Brokers is here to support your transition every step of the way. Contact us to determine if your business qualifies for free equipment and next‑day deposits.

Advanced Considerations: Compliance, Standards, and Optimization

Beyond selecting the right payment technology, small business owners must also navigate the complex world of compliance and cost optimization. As a dedicated merchant services provider for small business, we at The POS Brokers understand that staying compliant with industry standards is essential for secure, reliable credit card processing for small business. This section explores key regulations and practical optimization strategies that can help protect your business and improve your bottom line.

The following table outlines essential standards and resources every small business merchant should understand.

| Platform | Ideal Business Type | Key Features | Hardware Options | Cash Discount Compatibility |

|---|---|---|---|---|

| Clover | Retail, full‑service and counter‑service restaurants, service providers | App market, inventory management, tableside ordering, loyalty programs | Station, Mini, Flex, Go; mobile and countertop terminals | Yes, with compliant apps and configuration |

| Lavu | Full‑service restaurants, bars, nightclubs | Advanced floor plans, menu engineering, iPad‑based POS, offline mode | iPad kits, printers, cash drawers, kitchen display systems | Yes, via integrated processing rules |

| Revel | Enterprise‑scale retail, quick‑service restaurants, hospitality | Scalable platform, customizable UI, enterprise reporting, multi‑store management | iPad‑based terminals, self‑service kiosks, kitchen displays | Yes, with configuration support |

| ShopKeep (now Lightspeed) | Independent retail, boutiques, cafes | Cloud reporting, integrated payments, e‑commerce add‑ons, simple setup | iPad and tablet registers, barcode scanners, receipt printers | Supported with third‑party cash discount applications |

| SmartSwipe | Mobile vendors, pop‑up shops, service businesses on the go | Card reader for smartphones, mobile app, contactless payments, fast setup | Compact swiper/reader, no countertop terminal needed | Not applicable; Simple mobile processing solution |

We help our clients maintain PCI DSS compliance through secure hardware and processing solutions that align with data security requirements. For businesses processing ACH payments, adherence to NACHA rules is equally critical. According to the U.S. Payments Forum, adopting EMV and contactless technologies enhances transaction security and customer trust. By partnering with The POS Brokers, small businesses throughout the US gain access to compliant systems and guidance.

Beyond compliance, optimizing your payment strategy can significantly reduce expenses. Our cash discount program for small business is one effective method: by shifting processing fees to customers who choose credit cards, you can offset costs while offering transparent pricing. This cost-saving cash discount program, combined with our competitive wholesale rates, helps improve profitability without sacrificing service quality.

For those rare instances where disputes arise, the CFPB provides an accessible consumer complaint filing system. As a government agency, the Consumer Financial Protection Bureau ensures your concerns are routed to the appropriate company and, if necessary, published in a public database to promote accountability. While our aim is to resolve issues directly, we also guide our clients to this trusted resource for additional peace of mind.

Our team not only equips you with top-tier POS systems but also guides you through compliance and helps implement a cash discount program to lower your overall processing expense.

Frequently Asked Questions About Merchant Services

What does a merchant services provider for small business do?

We provide the tools and support small businesses need to accept card payments, manage transaction processing, and run POS hardware seamlessly.

How does credit card processing for small business work?

When a customer pays, the card network processes the transaction through interchange and processing fees. We pass through wholesale rates to keep your costs competitive.

What is a cash discount program for small business?

Our cash discount program offsets processing costs when customers pay with cash, while staying compliant with card brand rules.

Do you charge setup or cancellation fees, and can I get free hardware?

There are no setup or cancellation fees. Qualifying merchants can receive free or discounted Clover hardware when opening a new merchant account, a value we offer as your merchant services provider for small business.

Reach out to begin the qualification process.

Your Partner for Better Payment Processing

As a merchant services provider for small business, we believe in building lasting partnerships, not one-size-fits-all deals. We deliver credit card processing for small business across countertop, mobile, and e-commerce setups. Our no-cancellation-fee policy allows you to try our services without risk, and eligible merchants can qualify for free Clover placements. Our cash discount program for small business is a practical tool to offset processing fees, not a guaranteed saving. Ready to upgrade? Get the Best Credit Card Processing Solutions for Your Business today.

This article was researched and written with the assistance of AI tools.

Resources

- Step-by-Step Square Dashboard Password Reset Guide

- Five Troubleshooting Methods for Square Dashboard Login

- Recover Square Dashboard Access in Four Steps

- Payment Hardware Comparison for Business Optimization

- Five Tips to Regain Square Dashboard Access

- Clover Merchant Portal Guide for Business Management

- Embedded Payments Guide for POS Software Integration

- File Financial Complaints through CFPB Consumer Portal

- US Payments Forum Resources for Industry Standards